Ya gotta have a little drama on every trip to make it memorable, but today was a bit much, even for me! Here’s how it started.

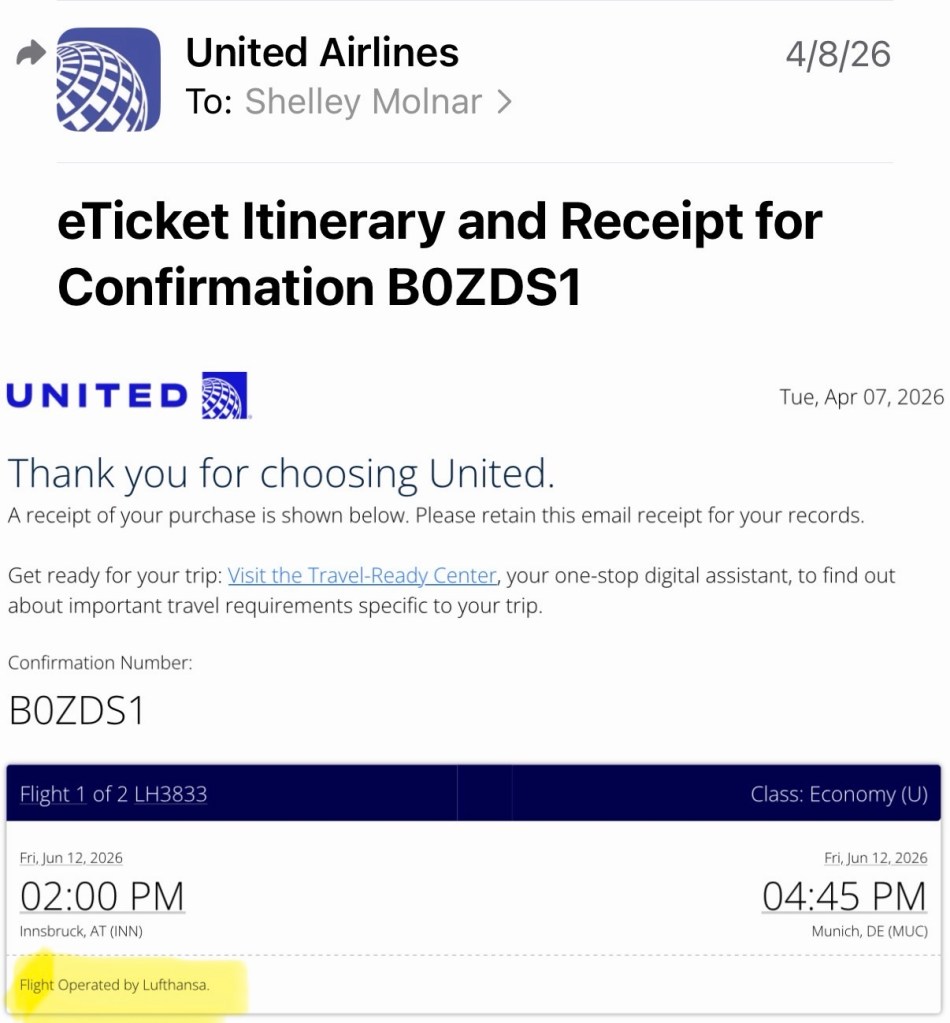

Originally, I thought I was FLYING from Innsbruck to Munich on Lufthansa, because that is what my United booking SAID.

I figured I’d have a leisurely breakfast, pack, then depart around 11 AM. To my surprise, my trip leader, Luca and fellow traveler, George informed me that there are no flights for the two hour and 45 minute trip. Furthermore, you only need to leave the hotel about 45 minutes to 1 hour before the bus departs.

Luckily, I was able to contact United to switch to the 10 AM bus. It only took about a half an hour on the phone and cost an additional $26, but it was worth it, because I had pretty much done everything worth doing in Innsbruck. Besides, the probability of rain that day was really high.

Four fellow travelers were on the 10 AM bus with me, so the hotel arranged for a van to transport us for the 12 minute drive to the airport. Yeah, even though we weren’t flying, we still had to go to the airport to catch the bus.

When I went to pay my share of the cost, I discovered my fanny pack, containing my passport, credit card, ATM card and cash was NOT around my waist. Pure panic!! I considered having a major meltdown, but decided to put that energy into devising plans B, C and D.

Luckily George was with me, so when I couldn’t figure out how to dial internationally, he called the hotel to ask them to check with the taxi company to ask whether it fell off in the taxi. Nope. Finally, I figured out the only other place it could be, was in my room, so the wonderful desk clerk at Stage 12 ran up and checked. Bingo.

I was so bloody lucky that she recognized that Jodie and Dan were in my travel group. She had called to reserve their taxi and knew they were traveling to Munich, so she gave them my fanny pack. When I met them at their hotel, Jodie told me that had I called five minutes later, they would have already left the hotel in their taxi. How lucky was I? How great were they?

Remember that movie “ Trains, Planes and Automobiles”? I felt like I had created my very own version, with me in a starring role —but I also added “Buses” to the mix. Why not?

Speaking of buses, this is something you don’t see every day— a bus driver smoking a pipe while driving!

When I arrived at the Munich Airport Hilton, the desk clerk allowed me to check in, using an image of my passport, stored on my phone. She wouldn’t accept the image of my credit card, but luckily I had stashed enough cash in my carry on. (George had very thoughtfully offered me Euros to tide me over, but my stash was adequate. )

By now, I am very aware of my many weaknesses, so I hide cash in multiple locations, specifically for times like this. I wish I could claim it was a rare occurrence, but it isn’t.

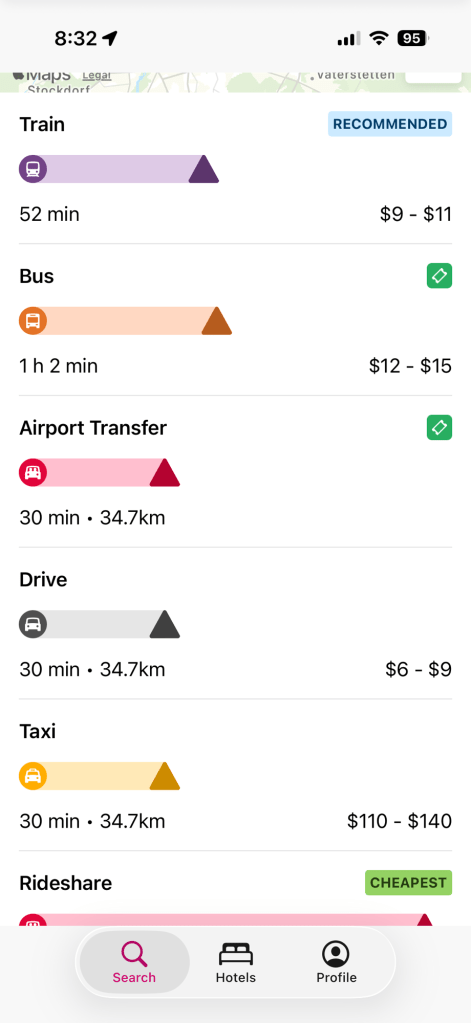

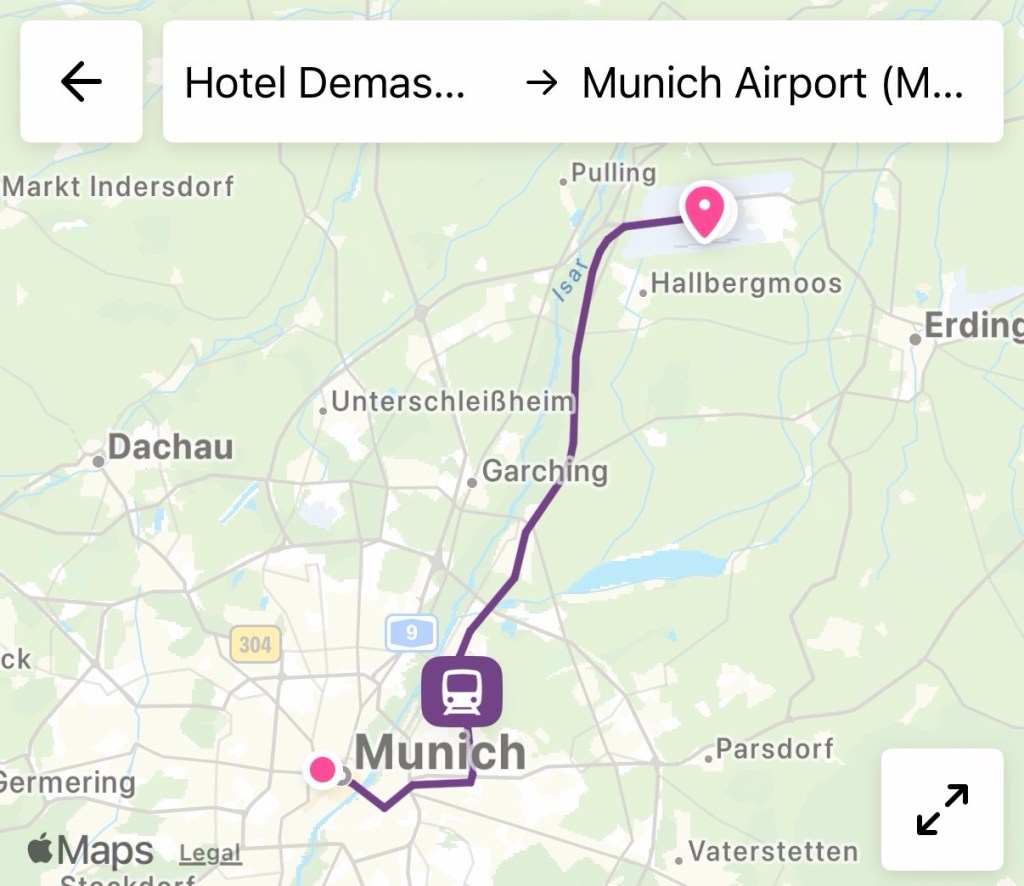

My next step was to figure out how to get to Jodie’s and Dan’s hotel in downtown Munich, which is approximately an hour away from the airport.

Rome2Rio app to the rescue! This free app listed all the different options for travel between the airport and the hotel, with the cost and the estimated time for each. For those who prefer a visual image, the app supplies a map that showed the distance between the two points.

Clearly The one way cost of $110 to $140 for a taxi was a non-starter, so instead I engaged in what OAT calls “Learning and Discovery”. I learned how to take the bus to the center and the train on the way back. ( The train is a much better option! No traffic. ). After giving me my fanny pack, Dan and Jodie walked me to the train station. This whole incident reminded me of the Beatle song “I get by with a little help from my friends”.

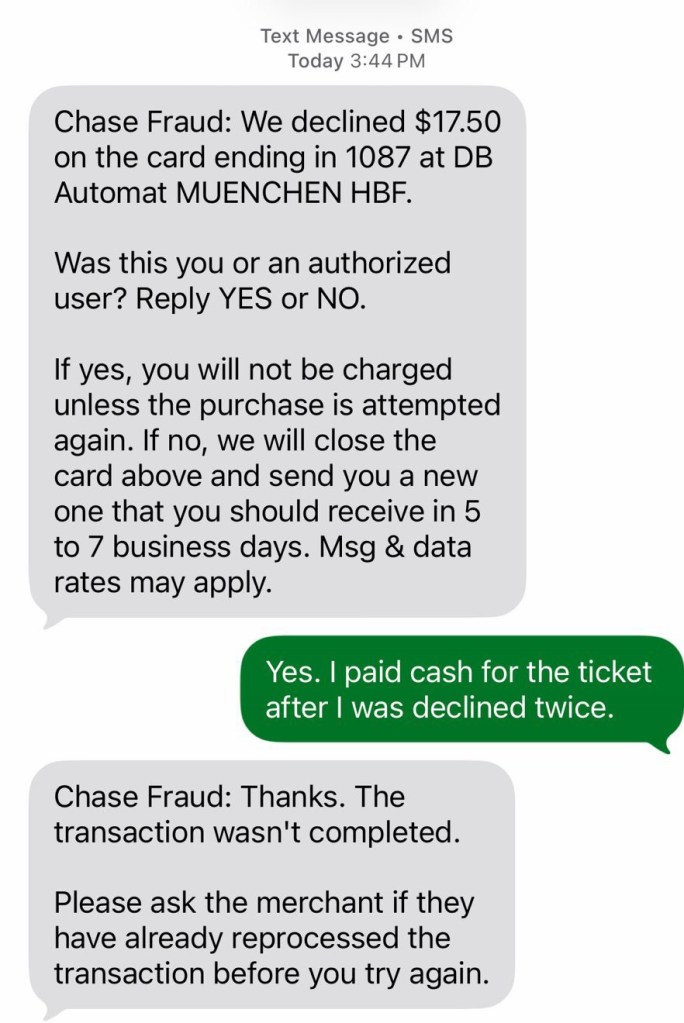

But wait! There’s more. I tried to use Apple pay at the airport ticket machine, and got rejected twice. Fortunately, I still had my last 20 Euros, so I paid cash.

On the train ride to the hotel, I got this text from Chase:

Alls well that ends well. The airport Hilton is beautiful,

the buffet dinner was delicious,

and I spent the rest of my evening thinking about how lucky I am to have had such an amazing trip with such wonderful new friends.

I’ll end this post with a line from the song Kay sent us all: “ Happy trails to you, until we meet again”. And I sure hope we do!